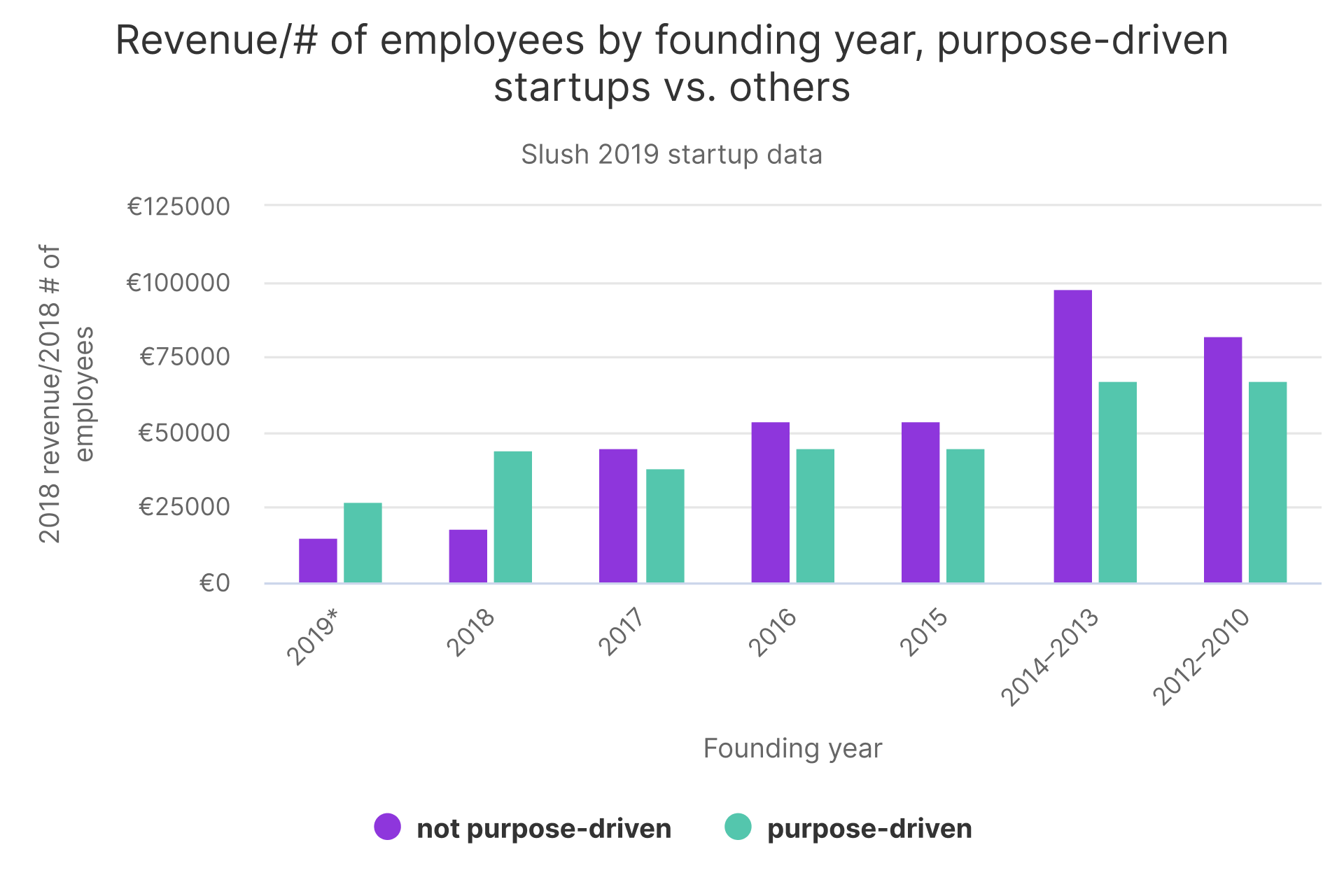

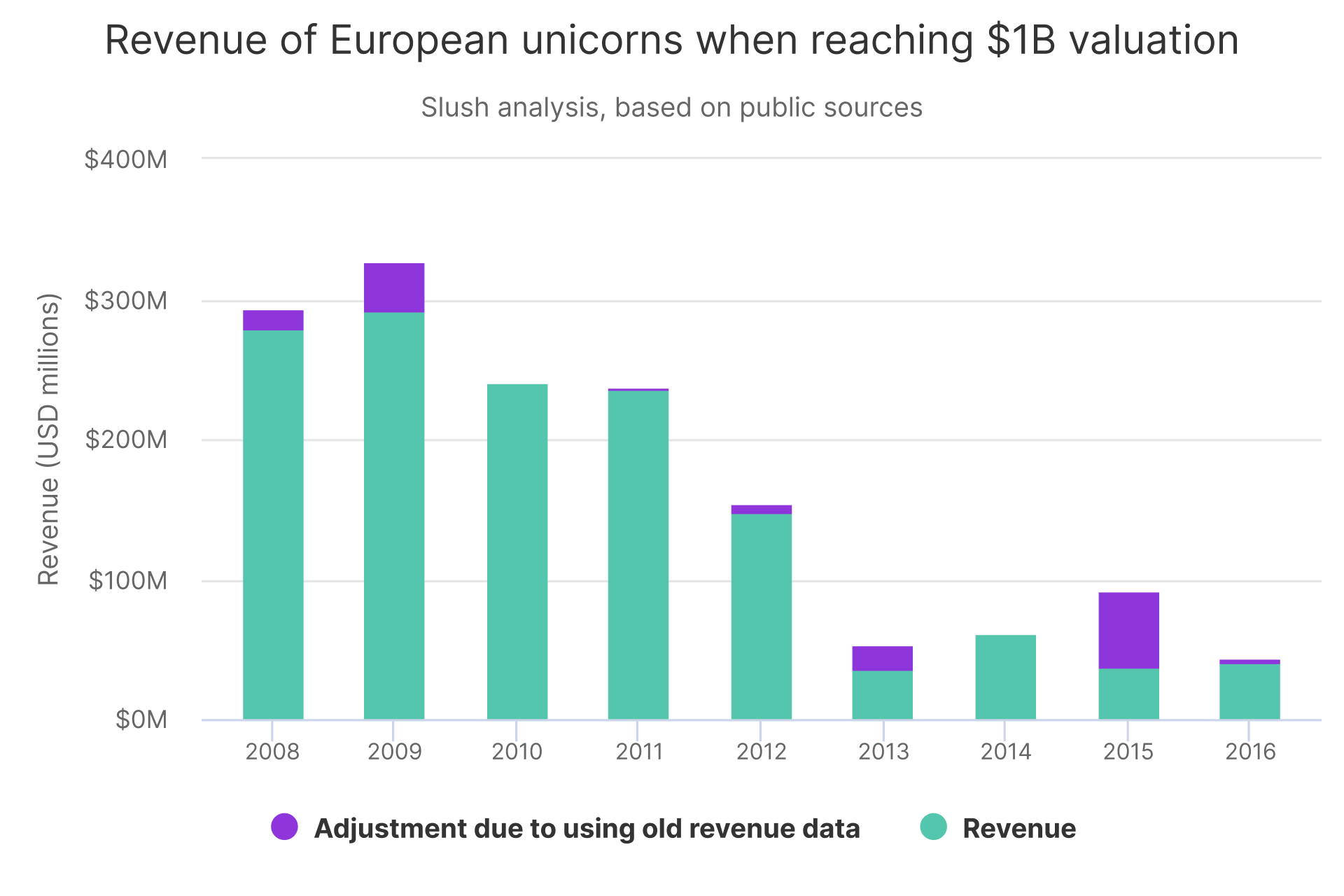

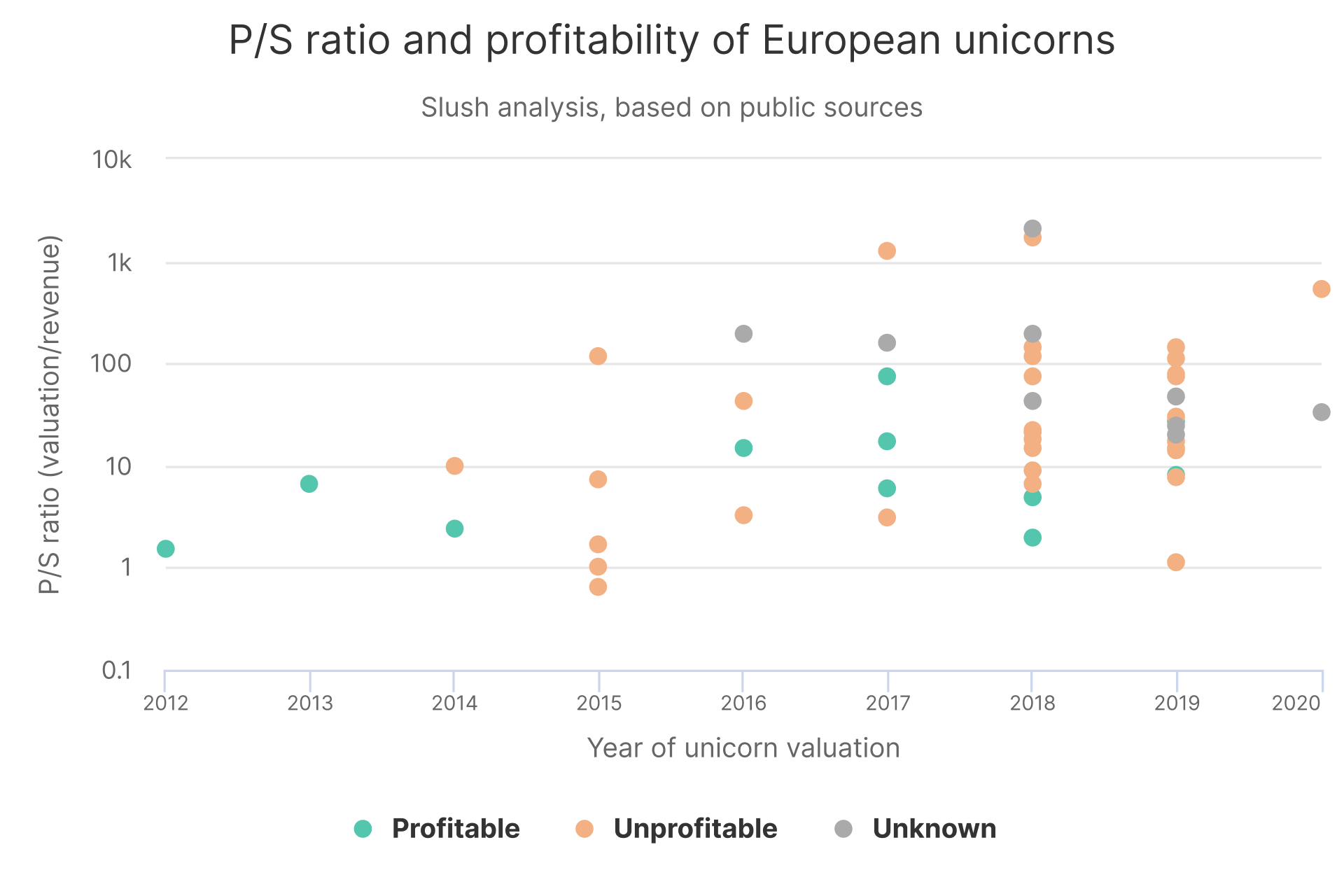

Eight companies turn a profit today at a P/S ratio of below 10 — a valuation that could be considered normal for a public company. Notably, two of these eight, Mojang and Outfit7, are gaming startups that didn’t raise significant external funding before their respective acquisitions. A third company, Eaton Towers, is private equity rather than VC-backed.

If venture-backed hypergrowth isn’t a proven path to sustained business value, why is it being pursued by founders and investors alike?

Firstly, both sides of the table will typically reap the benefits of a successful bet far before a company’s ability to produce long-term value is proven. Adam Neumann is a billionaire today, and if things had taken a slightly different course, the public market would have picked up the bill from his company falling from grace.

“There’s lot of talk behind the curtains along the lines of let’s get a C round in and get the fuck out. Strategic exits will always happen, but we should try building good businesses.”

– Founder

Secondly, the unusually high risk of VC as an asset class necessitates unusually high returns. This is heightened by the fact that, even in the best portfolio, the majority of young companies will fail. As a result, out of the dozens of companies that a typical fund will invest in, a few explosive successes will generate all returns.

Thus, VCs can’t afford modest, linear success. They push each portfolio company to work exponentially.

“For most entrepreneurs, your company is your only bet, whilst a VC has a number of portfolio companies, and want some percentage of those to succeed, and it’s almost irrelevant what happens to the rest. A VC wants to take loads of risk, and sometimes that might not be in the best interest of the company.”

– Founder

Thirdly, some of this haste to scale is a byproduct of the saturated digital world that we live in; one in which success is rare to come by, but astronomical when it happens. When companies rely on replicable IP for their unique selling proposition and anyone can scale a SaaS business infinitely from their garage, burgeoning traction needs to be defended at all costs. Often, the best defense mechanism is scale.

“Digitalization was the worst thing that ever happened to VC. Venture capital became an end to a means, and led to really unsustainable companies.”

– Founder

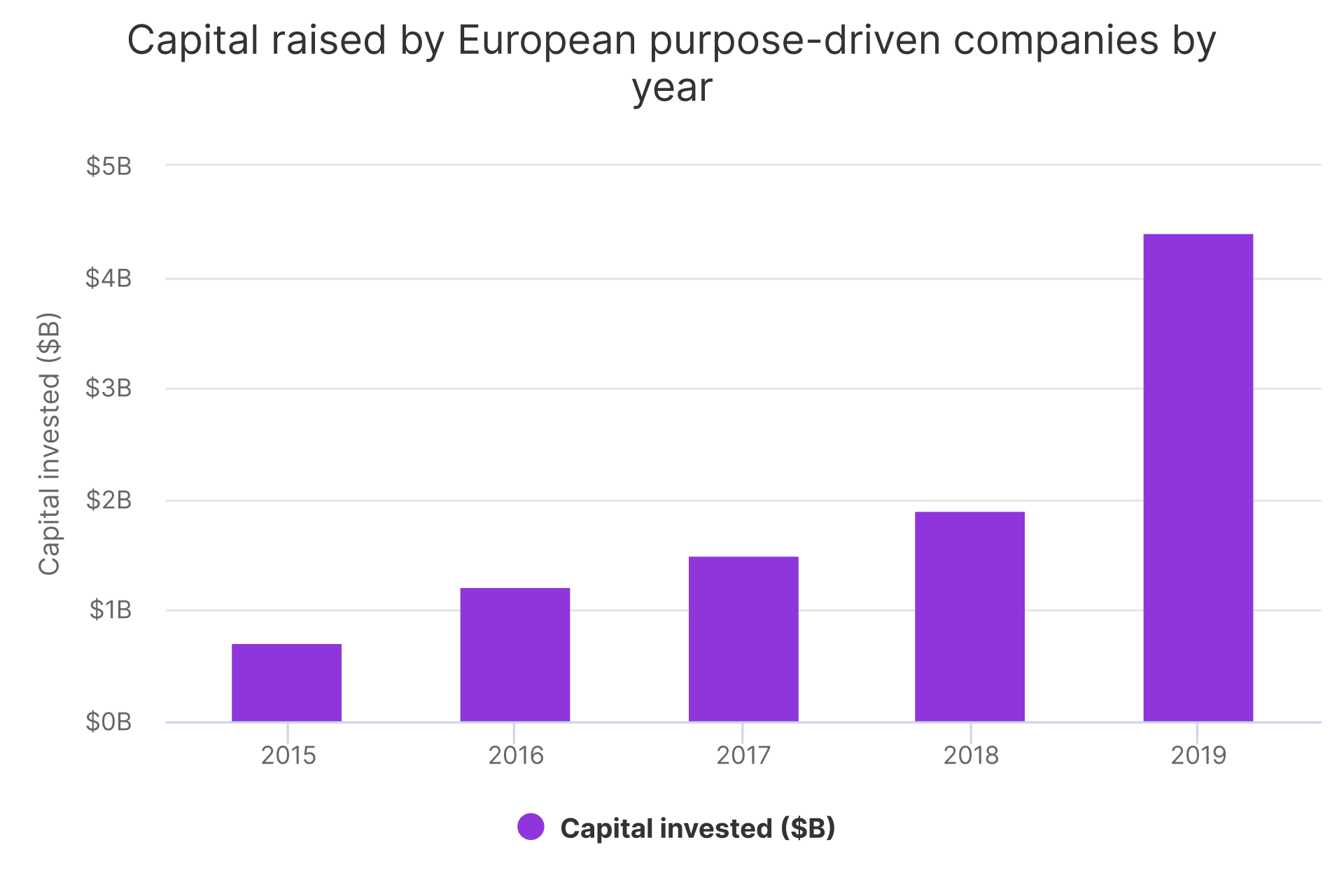

Arguably, venture capitalists are now finding the late-stage thesis so appealing that they’ve started turning away from the original purpose of the industry; unlocking the potential in unproven young ventures. As an indication of this, while total capital invested into European tech has more than doubled between 2014 and 2019, European seed funding has imploded over the past few years. The number of seed funding rounds was down 30% in 2019 from its 2016 peak, and total capital invested has stagnated.