Most of the innovations that will define the 2020s are already in development. Of course, many will still face a long and uncertain path before they are ready for implementation. A common way to categorize these kinds of industry-defining complex new innovations is deeptech. BCG and Hello Tomorrow define deeptech as tech that will have a big impact, take a long time to reach market-level maturity, and require substantial capital.

The European success stories of the past decade have mostly come from companies making incremental improvements within everyday problems, rather than those producing complicated, potentially revolutionary innovation. According to our analysis, among the 60 European unicorns founded since 2008, the most common industries are mobile, software, fintech, and healthcare. With the exception of healthcare, these industries don’t inherently lend themselves towards complex, meaningful technological advances.

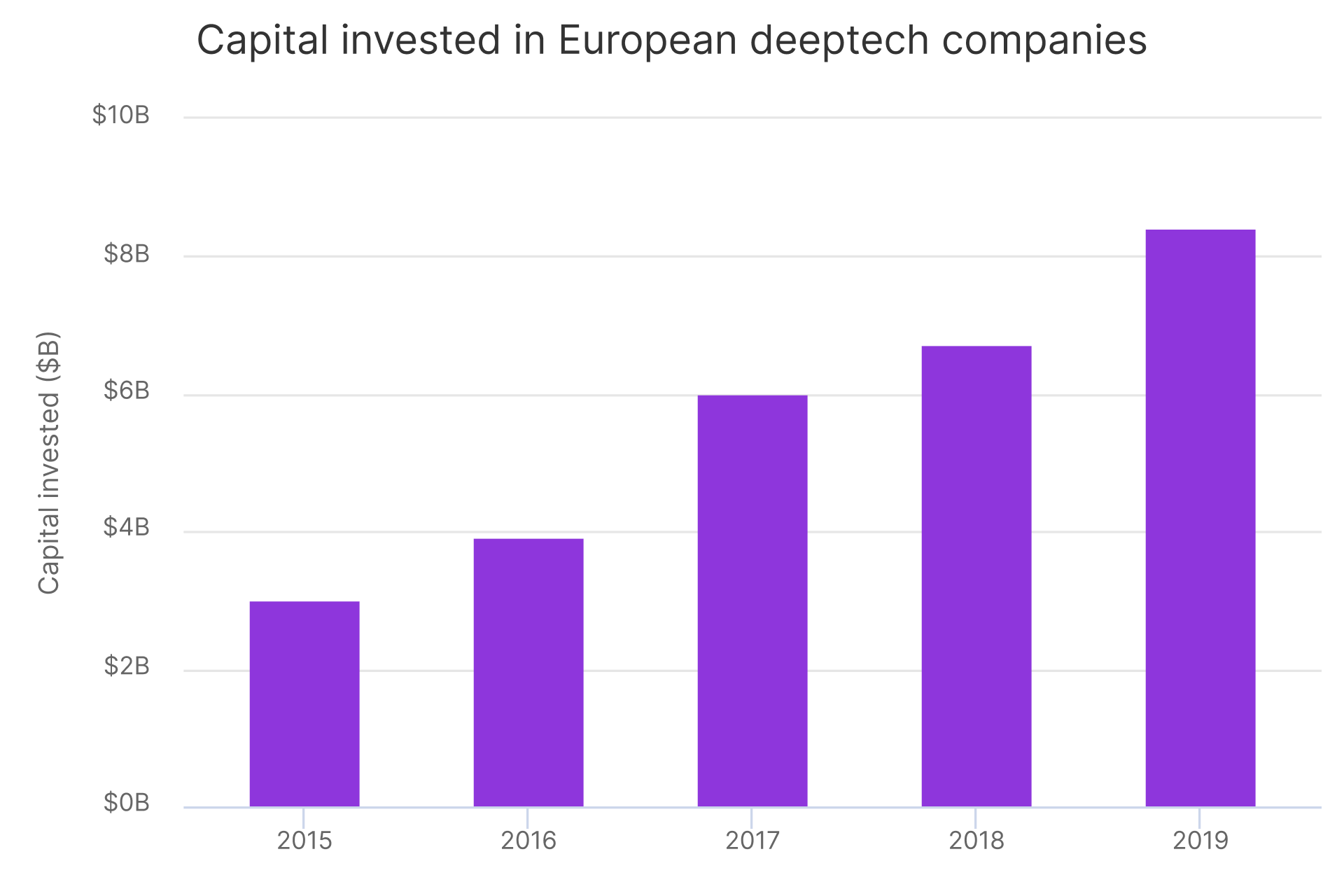

This shows that we’re far from unlocking the full potential of the ecosystem to produce revolutionary technologies.

“People are going to become a lot more interested in frontier science than finding another wearable.”

– Investor

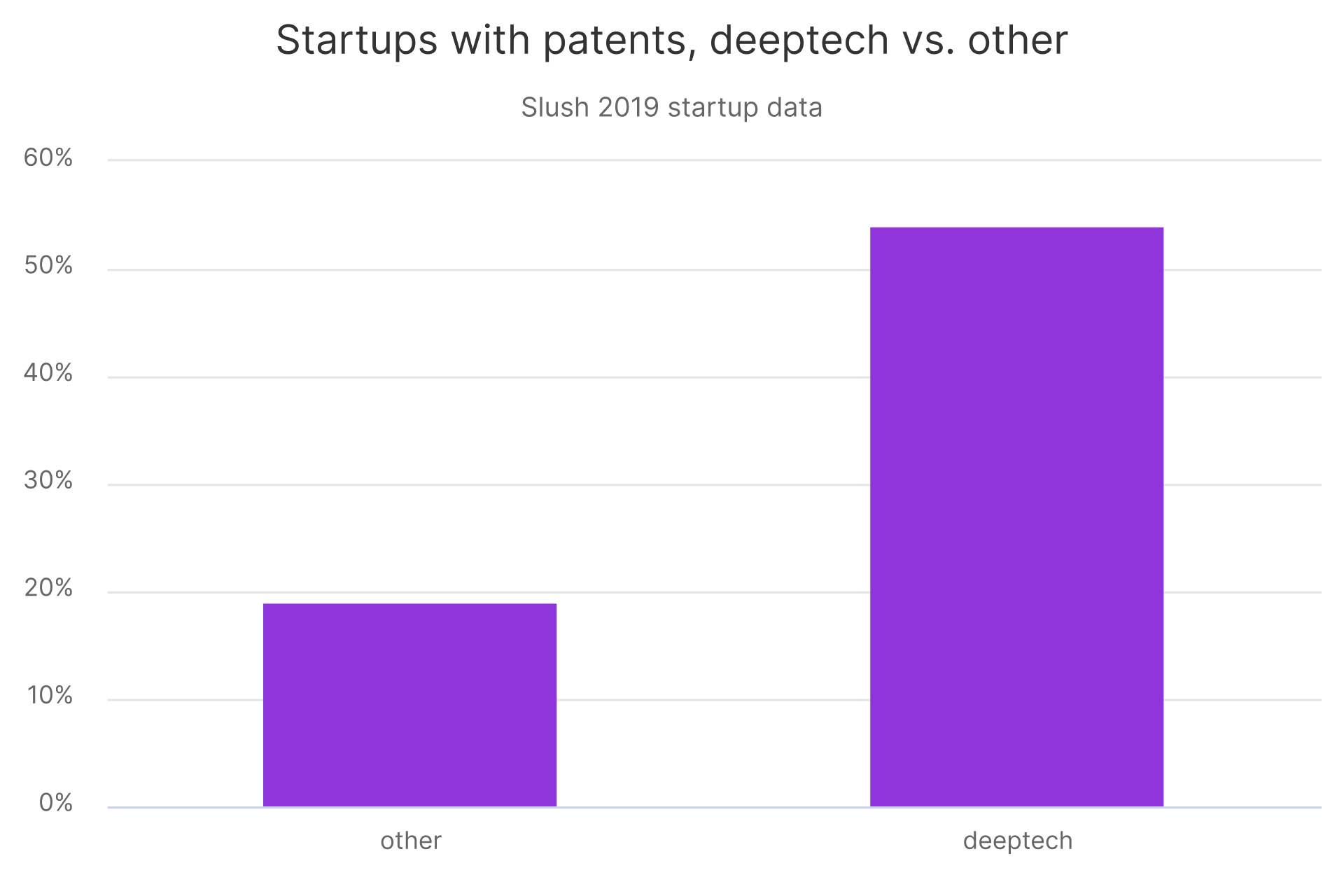

At Slush 2019, deeptech companies comprised 30% of all startups.

To recognize these, we used a combination of industry, technology, and keyword analysis, as well as manual scanning. Our aim was to find companies that leverage a novel, scalable, complex technology, or a significant innovation within an existing technology, as a core aspect of their offering. Additionally, this innovation needed to be the company’s own, and sold primarily as a product, rather than a service.

Arguably, the deeptech taxonomy is in and of itself a byproduct of the era of digitalization that we’ve been living through. When the infrastructure for our current, connected world was being built in the 70s, 80s and 90s, all tech was deeptech. Now, as opportunities and returns in the digital space are diminishing, more technically complex innovation is poised for a comeback.

This is important, because humankind desperately needs these kinds of technologies to address the existential threats that it faces. With the return to deep innovation, we need a world of effortless collaboration within and across different factions of society, where all lines of human ingenuity are exploited to the utmost.

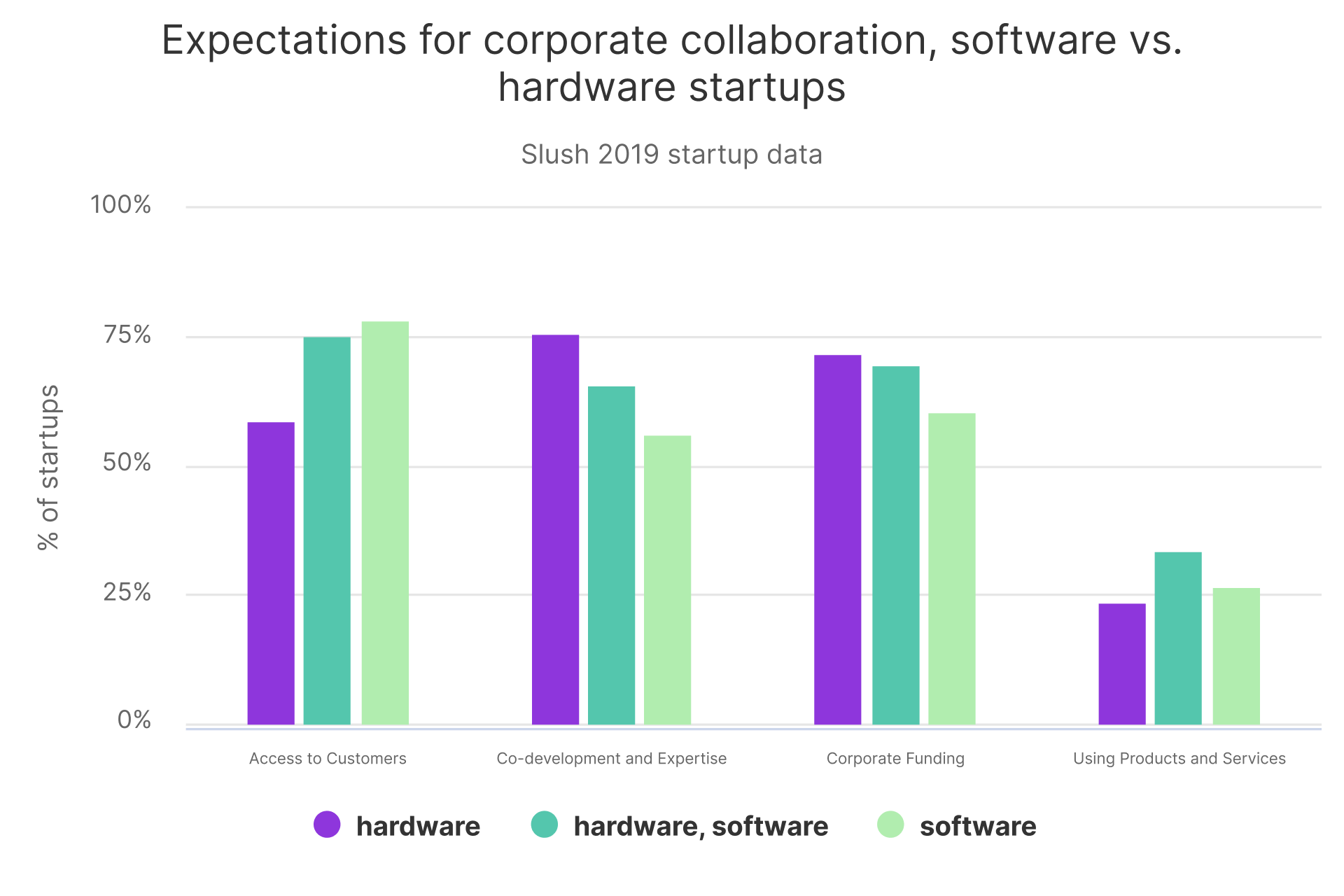

“If startups want to tackle the big, complex challenges that the world faces, like climate change, urbanisation and health, they can’t work on their own anymore. These problems require us to collaborate closely with corporations, governments and cities.”

– Operator