Leo Johnson

From wildfires in California to melting glaciers in Greenland, and from droughts in Africa to floods in Europe, society is already feeling the effects of the climate crisis. But the future impacts of planetary warming will be much more significant than those witnessed to date.

It’s a grim scenario that demands drastic action – an imperative reiterated by the latest United Nations Intergovernmental Panel on Climate Change (IPCC) report in August 2021. However, the good news is that technology to help tackle climate change is also advancing at pace. This technology is being developed by an expanding global community of climate tech companies that are attracting rapidly increasing interest and investment.

What’s the state of play?

Climate tech is a maturing asset class that PwC has spotlighted in a recent research study – State of Climate Tech 2021. However, before diving into the findings, let’s do a quick status-check.

As anticipated, COP26 generated a barrage of climate commitments. The international agreements to slash methane emissions and end deforestation were positive developments, as was the US-China cooperation agreement announced during the second week. Other steps forward included the launch of the Breakthrough Agenda to deliver clean, affordable technology worldwide by 2030, and the First Movers Coalition to help companies create markets for clean energy technologies. Both initiatives signal rising demand for more innovation by climate tech entrepreneurs and more investment in climate tech.

Whilst COP26 delivered significant progress in terms of commitments, the hard work is just beginning in order to deliver on these decarbonisation commitments. We’ve been here before: the Paris Agreement in 2015 to limit global warming to 1.5°C saw governments and businesses worldwide pledge to meet long-term net-zero goals. But PwC UK’s Net Zero Economy Index shows decarbonisation simply isn’t happening quickly enough – a view backed up by the Climate Action Tracker (CAT), which calculated towards the end of COP26 that we’re heading for 1.8°C of warming even if all pledges, long-term targets and net zero targets are achieved.

Hardly surprising then that many participants feel the window to keep within the 1.5°C target is closing fast. PwC’s Net Zero Economy Index agrees: it suggests that a decarbonisation rate of 12.9% is now needed to deliver 1.5°C – that’s five times the rate achieved in 2020, and eight times the global average since 2000. It’s a huge ask. However, there is room for optimism when it comes to innovation and climate tech. As Larry Fink, CEO of BlackRock, has commented, the next billion-dollar startups will be in climate tech.

It’s a much-needed rallying call. While countries accounting for around 90% of global GDP have set net zero targets, most are behind schedule, despite the COVID-19 pandemic dampening effect on emissions. Meanwhile, the private sector is stepping up with a surge in climate pledges, as more and more companies join the Race to Zero campaign, or commit to reduce emissions through the Science Based Targets initiative. Over half of the sectors making up the global economy have pledged to halve their emissions by 2030. But more concrete action is needed to get there.

Two reasons for optimism: breakthrough climate technologies…

But against this apparently challenging background, there are two reasons to be optimistic – and they both underline the importance of the innovation ecosystem that’s grown up around Slush, underpinned and supported by VC and Private Equity (PE) investors. The first reason? A rising generation of climate tech startups are applying digital innovation to address emission intensive ways of operating and doing business, and opening the way to new business models with huge breakthrough potential in addressing climate change.

The economy-wide change, enabled by emerging technologies, is set to be transformational. Take the emission intensive sectors of transport, energy and food, that collectively generate around 50% of carbon emissions globally. In combination with expanding and increasingly cheaper renewable energy from solar and wind, and ongoing advances in battery capabilities, the new climate technologies have clear potential to outpace and ultimately replace the legacy fossil-fuel-based centralised models in all of these industries. In doing this, climate tech would be delivering dual economic and environmental benefits. While renewables were once seen as a pricier alternative only for the environmentally conscious, they are now officially the cheapest form of electricity in history.

The opportunity for climate tech to help move the dial has been further underlined by the International Energy Agency (IEA), which states in its report Net Zero by 2050: A Roadmap for the Global Energy Sector that ‘in 2050, almost half the [forecast emissions] reductions come from technologies that are currently at the demonstration or prototype phase.’ The reality is that these technologies exist but have not yet reached scale – and society needs them to reach scale as quickly as possible. It’s a scenario that plays to the strengths of VC, which has a successful track record in scaling up technology rapidly.

What kinds of technologies could help tackle climate change? In the UK alone, we’re seeing startup-driven innovations ranging from Deep Branch Biotechnology’s carbon-negative protein production in collaboration with the Drax power station in North Yorkshire, to First Light Fusion’s research into inertial confinement fusion. Other areas of rapid progress range from precision fermentation – bringing together artificial intelligence (AI), machine learning and the cloud with modern biotechnologies like genetic engineering, synthetic biology and metabolic engineering – to electric autonomous vehicles and vehicle grid integration.

…and rising VC interest and involvement…

The rapid advance of climate tech is a significant piece of good news as the world faces the climate challenge. The other is the rising impact of the venture capital and private equity community, as VCs’ interest and involvement in climate tech rises rapidly. With new use case opportunities and innovations to capitalise on continuing to emerge, regulatory systems are starting to reflect and align with governments’ net zero commitments – a shift evident both among formal regulators and quasi regulators, including central banks, and in reporting disclosure requirements.

The effect is to open up opportunities for other VCs to come in and invest. And they’re doing so in increasing numbers – playing a critical role in taking climate tech startups to the point where they can have a global impact. VCs are doing this by providing the seed, angel and Series A and B funding that may enable climate tech innovators to get through the so-called ‘valley of death’ that still exists between startup status and scale.

…are triggering a sustained surge in investment

Against this background, PwC’s State of Climate Tech 2021 report highlights the pace at which VC investment is increasing, and the resulting energising effects on climate-focused innovation. According to the 2020 report, as recently as 2013, global VC investment into climate tech was just US$418 million per annum. From that base it rose to US$16 billion per annum in 2019, as investors in mainstream sectors such as real assets began to pour more funding into decarbonisation. This sustained surge in climate tech investment reflects interest from a wide range of investor types: PwC’s 2021 report has identified more than 6,000 unique investors, ranging from VCs, PE and corporate VCs to angel investors, philanthropists and government funds. Together, these diverse investors have funded over 3,000 climate tech startups between 2013 and H1 2021, and around 2,500 of them were active between the second half (H2) of 2020 and the first half (H1) of 2021. However, the average number of deals per investor remains relatively low, suggesting that the majority are just dipping their toes as climate tech matures as an asset class.

But, more positively, this maturation is advancing apace – with 2021 marking a tipping-point as overall investment goes into overdrive. The report found that US$87.5 billion poured into climate tech over H2 2020 and H1 2021. The first half of 2021 alone delivered record climate tech investment levels, totalling in excess of US$60 billion: that’s a 210% year-on-year increase, and nearly ten times the level five years before. The average deal size has also leapt in H1 2021, nearly quadrupling from the previous year to US$96m. This is partly due to megadeals – investments worth US$100 million or more – becoming increasingly common as larger players escalate their efforts to reach their net zero targets. From 70 megadeals in the entirety of 2019, their number jumped to 120 in the first half of 2021 alone.

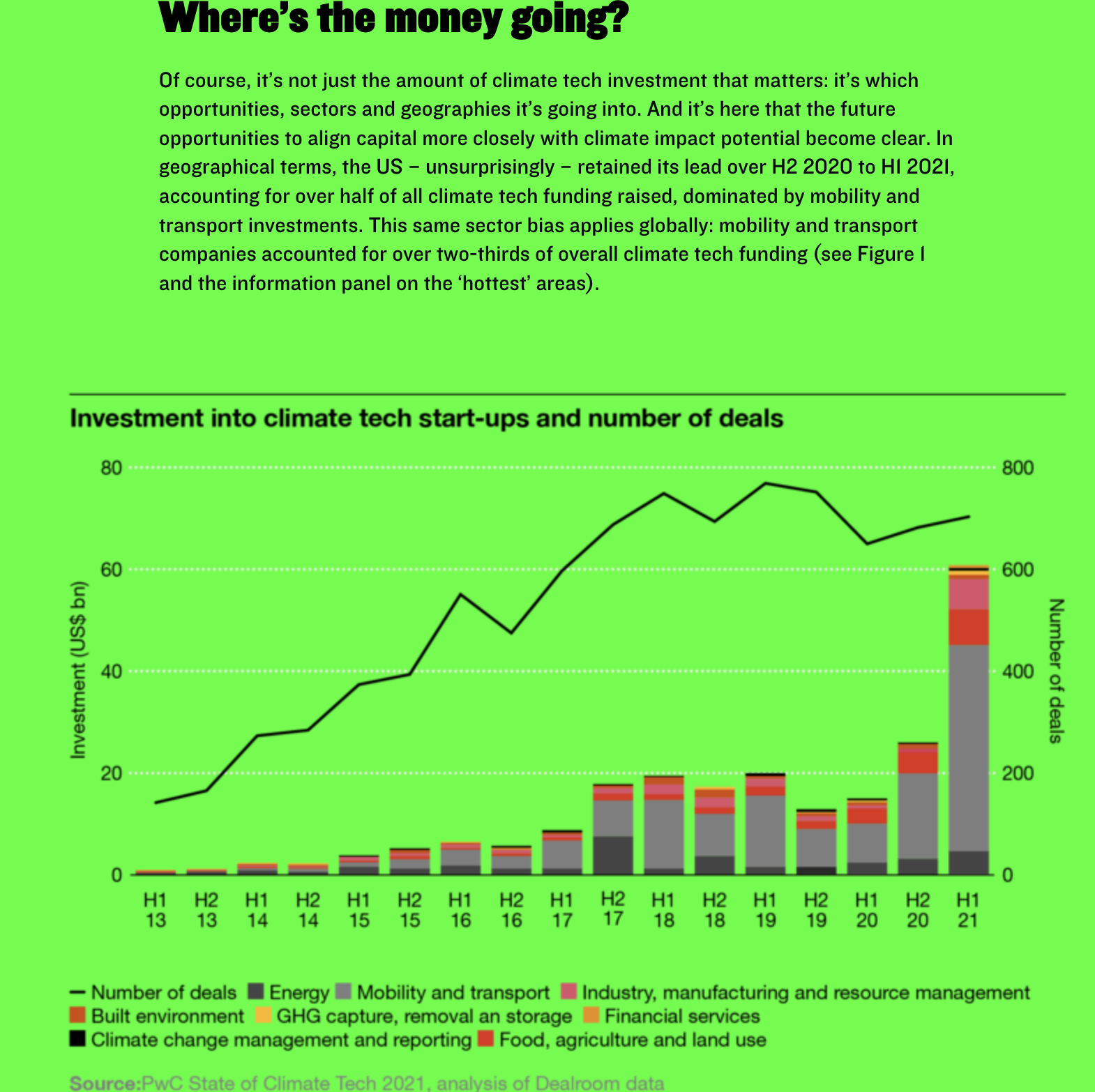

The dominance of mobility and transport mirrors a wider trend: that a handful of technology areas, seen as ‘safer’ and more certain in terms of returns, are still attracting the majority of early-stage climate tech investment.

In PwC’s view, the VC industry needs to look at climate tech more holistically, and uncover the deep cross-sectoral decarbonisation opportunities that will mark out the future ‘Gigacorns’. The bottom line is that businesses, governments and society need to remove carbon emissions from all stages of the value chain – and startups tackling mitigation needs that are as-yet unmet offer VCs the chance to create both commercial and environmental value. The accompanying box-out lists some of the nascent technology areas where future funding will enable breakthrough innovations and accelerate decarbonisation in more sectors.

The irreversible transition from a fossil-fuel model to a lower- or net zero economic order is underway. The breakthrough technologies needed to enable the journey are emerging – and VC investors are uniquely placed to support the transition while also generating substantial financial returns. To realise it, society must scale up climate tech – through policy, through capital and through industry collaboration. And society must do it now, for the future of mankind, together.

PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details.