Susan Hyttinen | Mikko Mäntylä

Corporate-Startup Collaboration is more relevant than ever and has a lot more to it than just investments. We looked at 3,500 startups and 1,000 investors in the Slush database to learn some more about these entanglements – here’s what we found out.

Corporate-startup cooperation has progressively become more topical in past years. While a lot of the recent interest in corporate-startup collaboration has been focused on investments and acquisitions, there are other important ways in which corporates and startups can be useful to each other. For example, corporate partners are often enlisted when startups need help in expanding to new markets and working on their product.

In this article, we will take a closer look at what the data has to say about the inner workings of startup-corporate entanglements. While we discuss investments extensively, we’ve also looked at corporate-startup collaboration in a more comprehensive manner. There are some interesting dynamics at play; expect to learn about who’s particularly dependent on corporate cooperation, at what stage corporates are likely to invest, and how corporate investors fare in terms of gender diversity metrics, among other things. Let’s jump in!

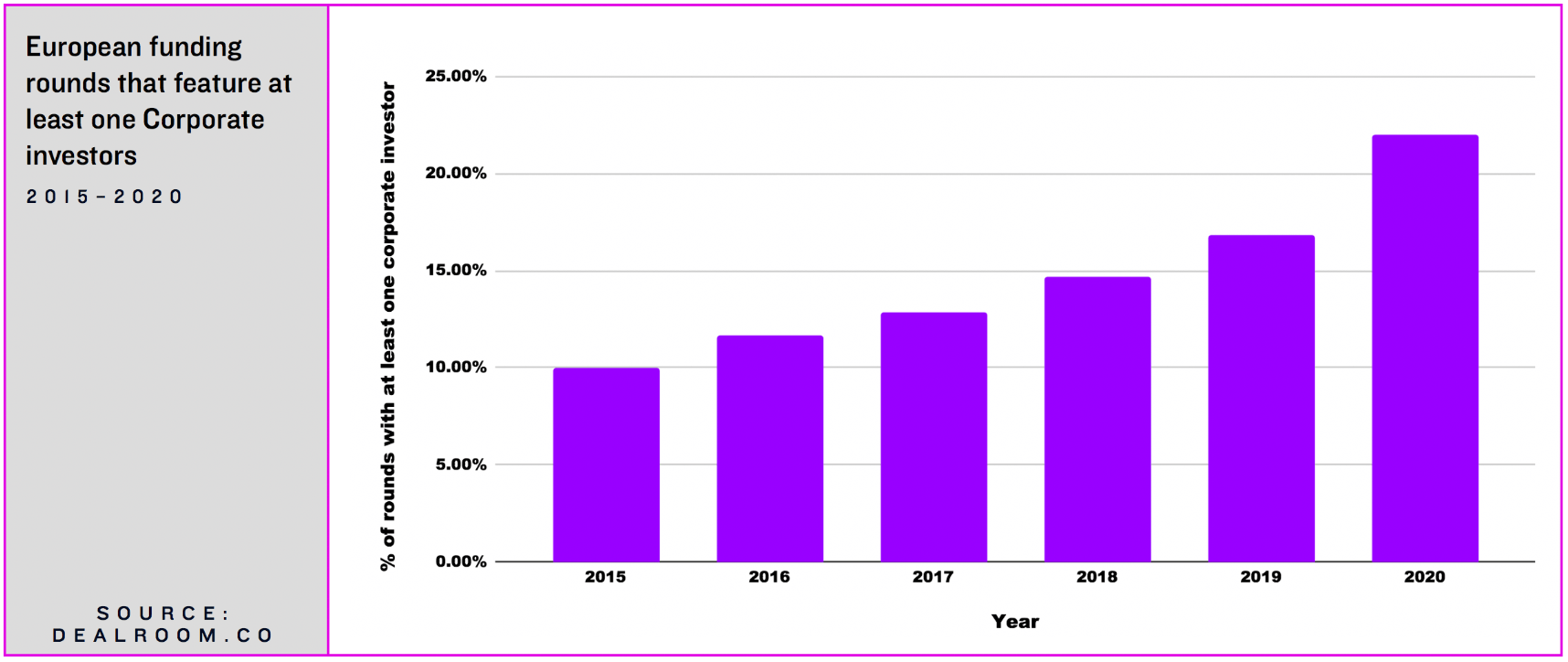

#1 The ‘I knew this already’ point – the share of European funding rounds that feature a corporate has exploded

In recent years, corporate investors have established themselves as an integral part of the European funding landscape. Since 2015, the share of European funding rounds that feature at least one corporate investor has more than doubled. Last year, corporates participated in more than one in five European rounds.

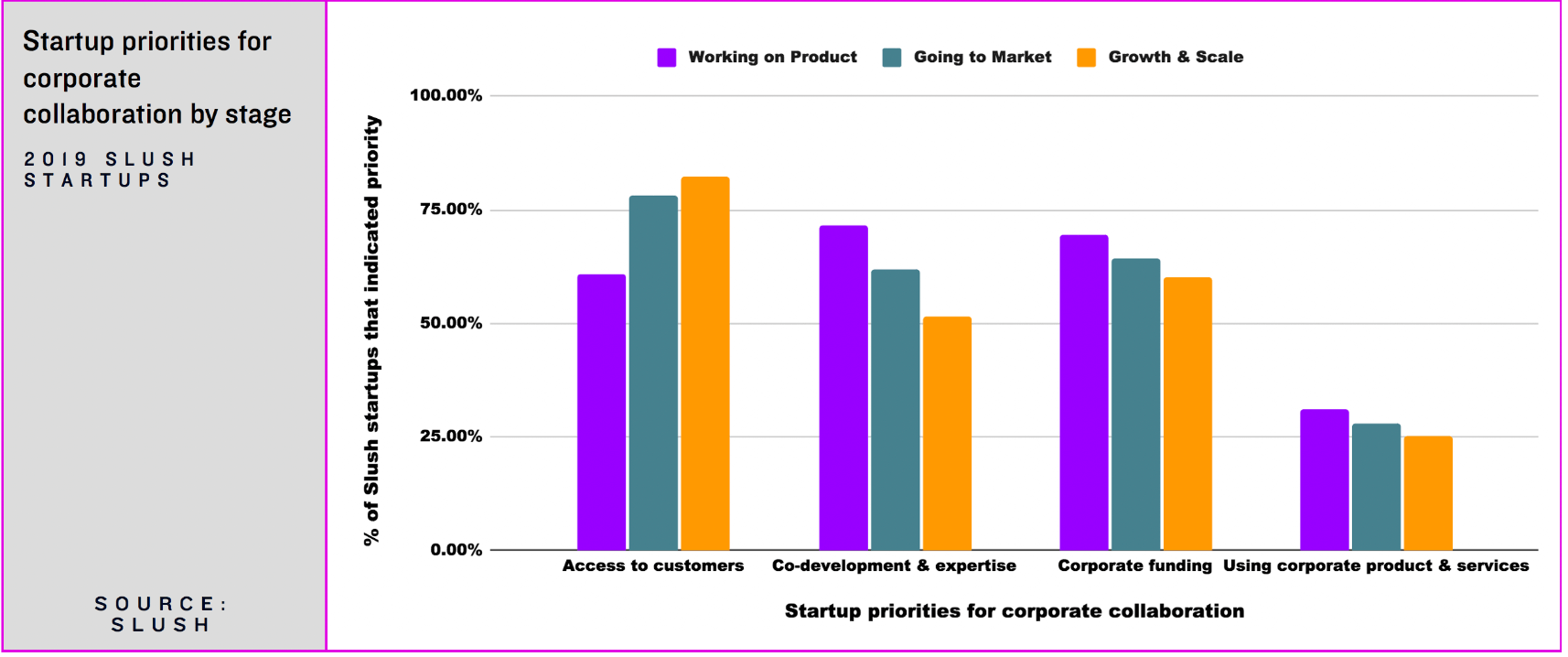

#2 Corporate-startup collaboration is about a lot more than cash – and startups are the first to voice this

Surveying over 2,000 of the startups at Slush 2019 on their wishes for corporate-startup collaboration, we found that, surprisingly enough, funding does not make it to that top step of the podium for any stage of startups.

While building their product, startups are primarily looking to leverage corporate expertise for co-development efforts. As they start focusing on scale, startups’ first priority becomes accessing customers through their corporate partners.

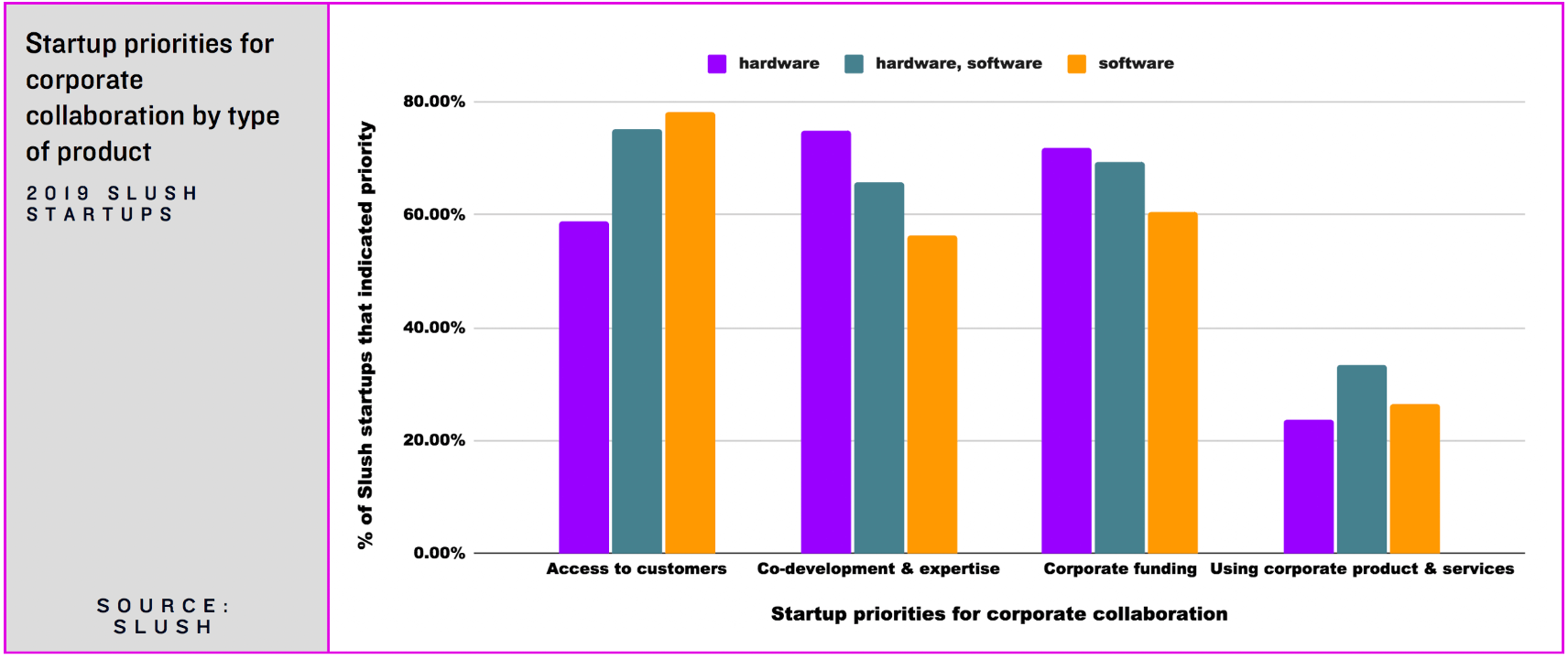

#3 Hardware startups are particularly dependent on corporate expertise – and cash

Much like the way startups wish to engage with corporates is stage-contingent, it is affected by the type of product the startup in question is building.

Specifically, while the overarching priority for software startups is access to customers, hardware startups actually value co-development and expertise over other modes of collaboration. What’s more, hardware startups are much more likely to be on the lookout for corporate euros.

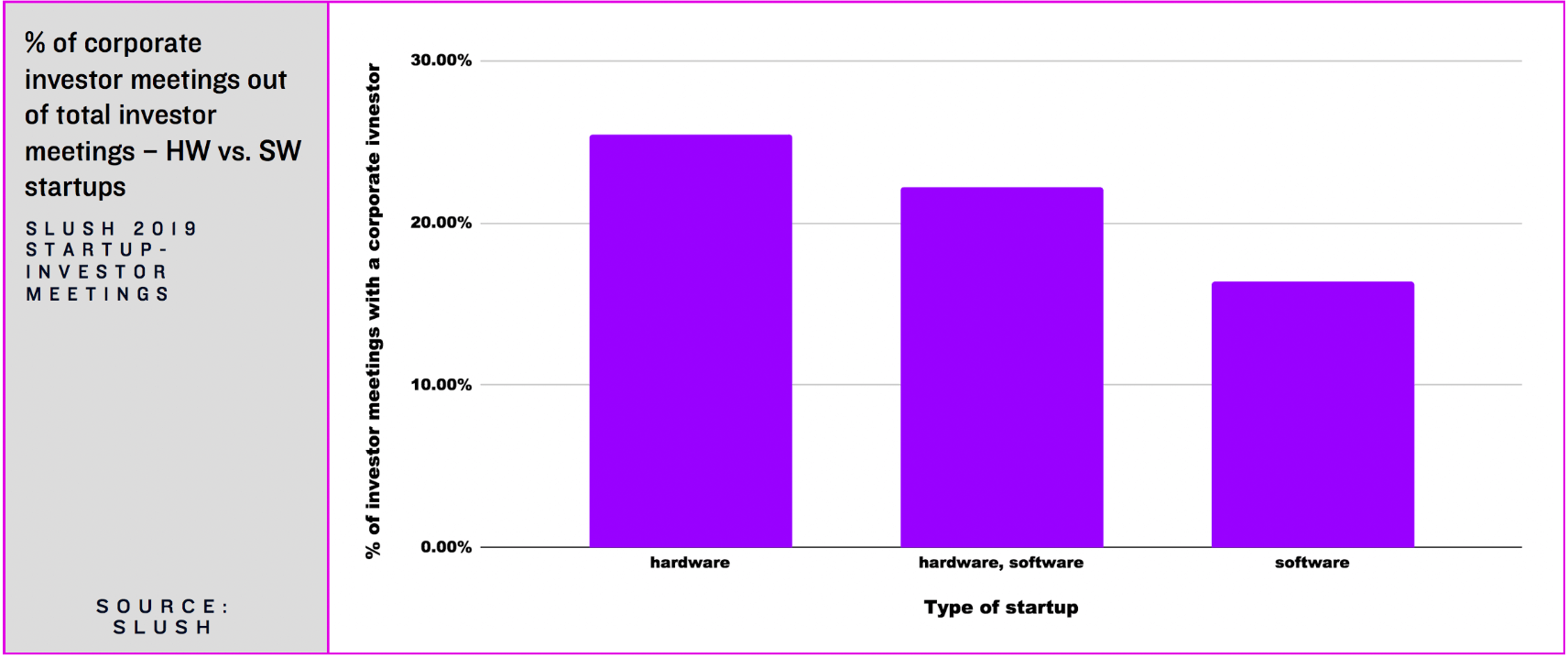

In terms of investments, hardware startups’ appreciation for corporations seems to be reciprocated. Corporate investors at Slush 2019 were almost 2.5x more likely to invest in pure hardware products than VCs. As one could expect, CVCs are better placed to judge the technical risk involved in hardware bets (at least when investing within the domain of their parent company), as well as more able to accept the long time horizon involved. After all, most corporate investors don’t face the pressure of external Limited Partners (LPs), or even a fund structure at all.

This all, in turn, is appealing to startups. As a result of it all, 25% of hardware startups’ investor meetings at Slush 2019 were with a corporate investor, compared to 16% of those that software startups took. It’s a match!

#4 Half of corporate investors consider strategic alignment a necessity

Since most corporate investors manage a parent company’s money – either directly or through a single-LP fund structure – strategic incentives that speak to broader corporate objectives are clearly part of the investment equation.

However, based on what we learned from the corporate investors at Slush 2019, this may be less common than one would anticipate. Only 47% of corporate investors reported that their deal flow needs to be directly connected to their parent company’s business or product. Corporate investors may be more versatile creatures than we give them credit for.

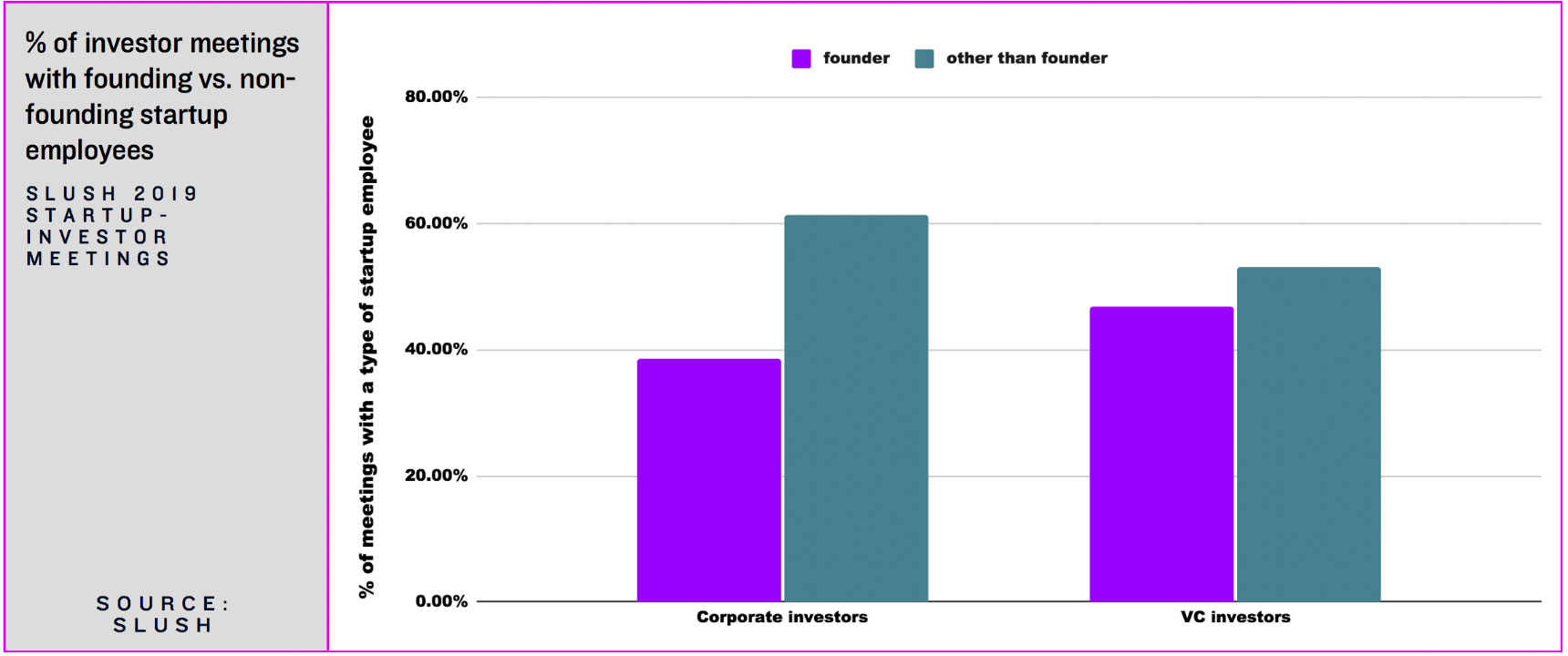

Nevertheless, compared to VCs, it’s clear that corporate investors act on a broader set of priorities. This is reflected in the profiles of startup employees that they meet with. At Slush 2019, 61% of meetings between corporate investors and startups were with a non-founding employee, compared to 53% of VC meetings. Corporate investors are talking to a more diverse mix of startups’ staff – including technical experts, salespeople, and partnerships managers.

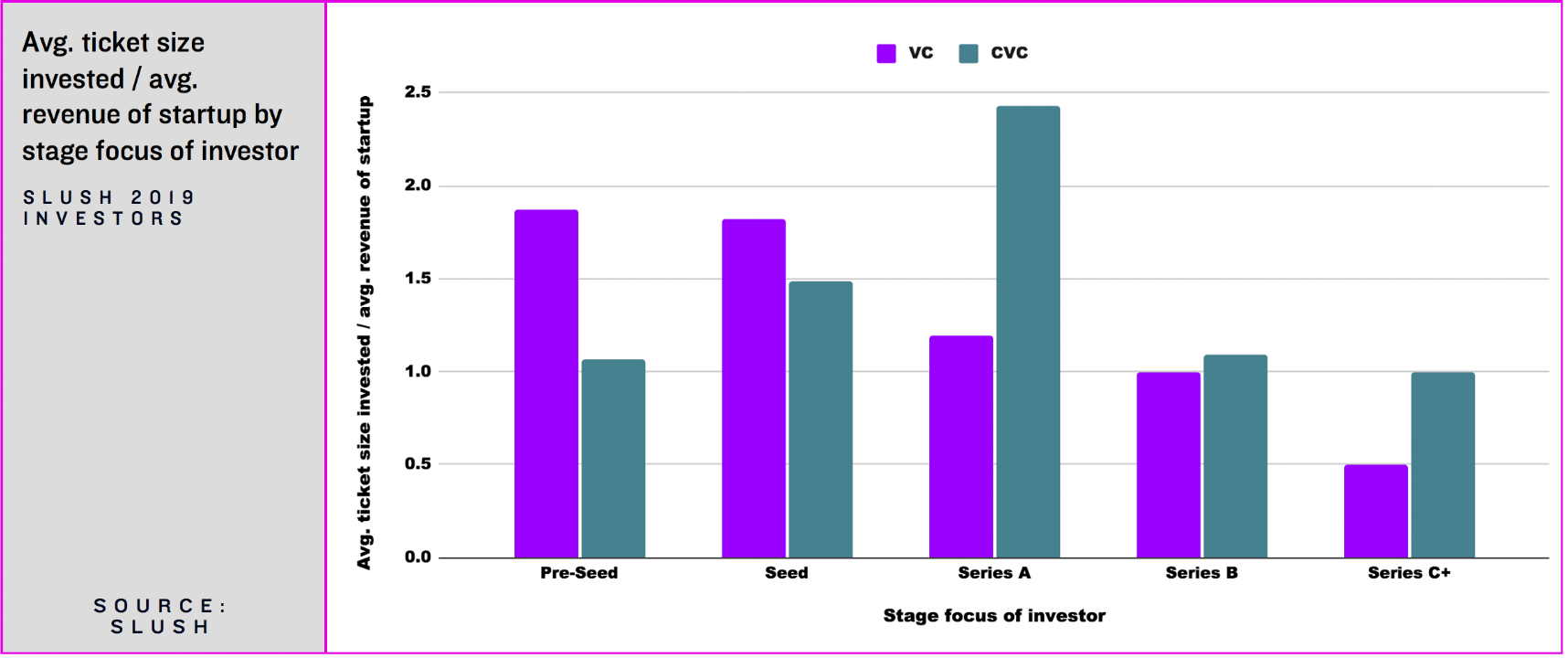

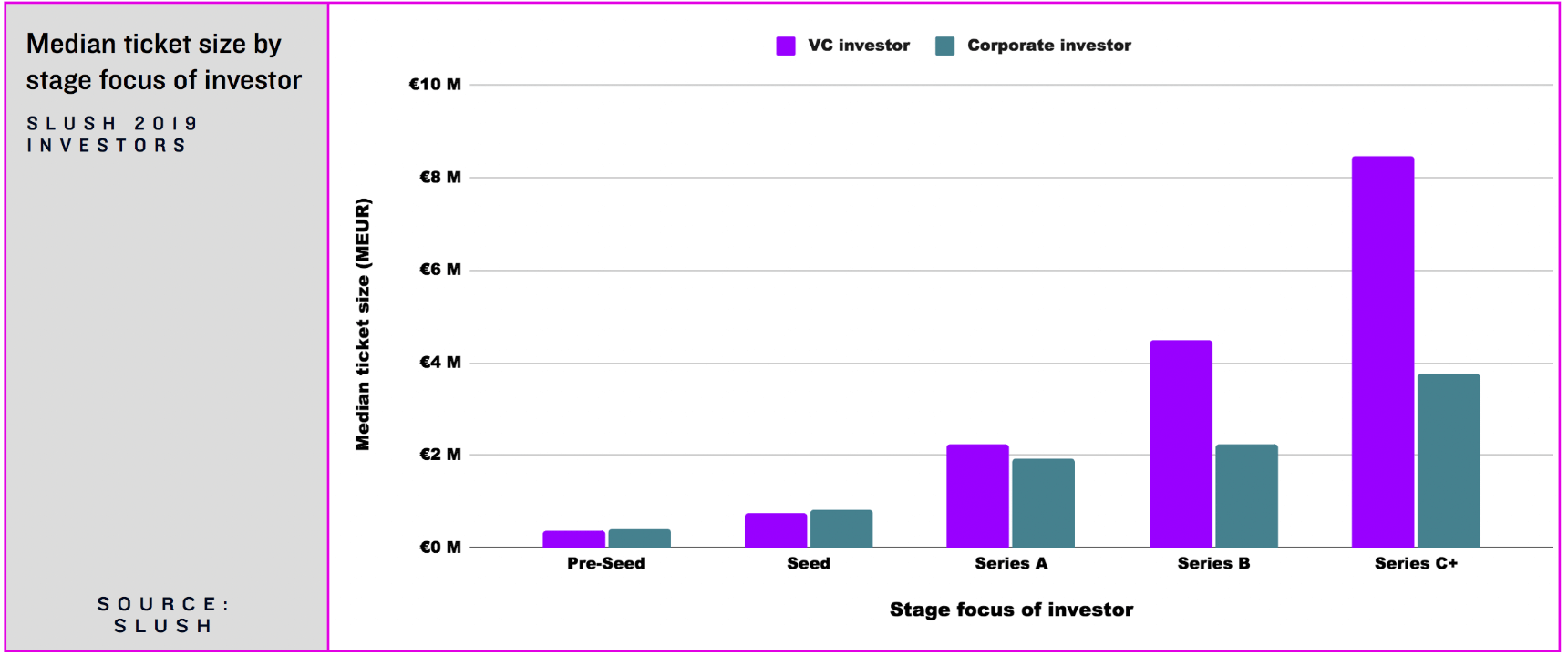

#5 As synergies emerge, corporate investors are ready to give out higher valuations

The fact that corporates invest to leverage technical expertise or to set themselves up for an acquisition carries synergies that allow them to value companies higher than VCs.

Data we collected from the investors at Slush 2019 suggests that such synergies only emerge at Series A and beyond. Looking at the revenue that investors expect as a share of the tickets they write shows that, while corporates are valuing companies more conservatively at the pre-seed and seed stage, they become significantly more generous than VCs beyond Series A. Of course, this analysis doesn’t account for equity received, but any differences therein are unlikely to be big enough to explain the gaps.

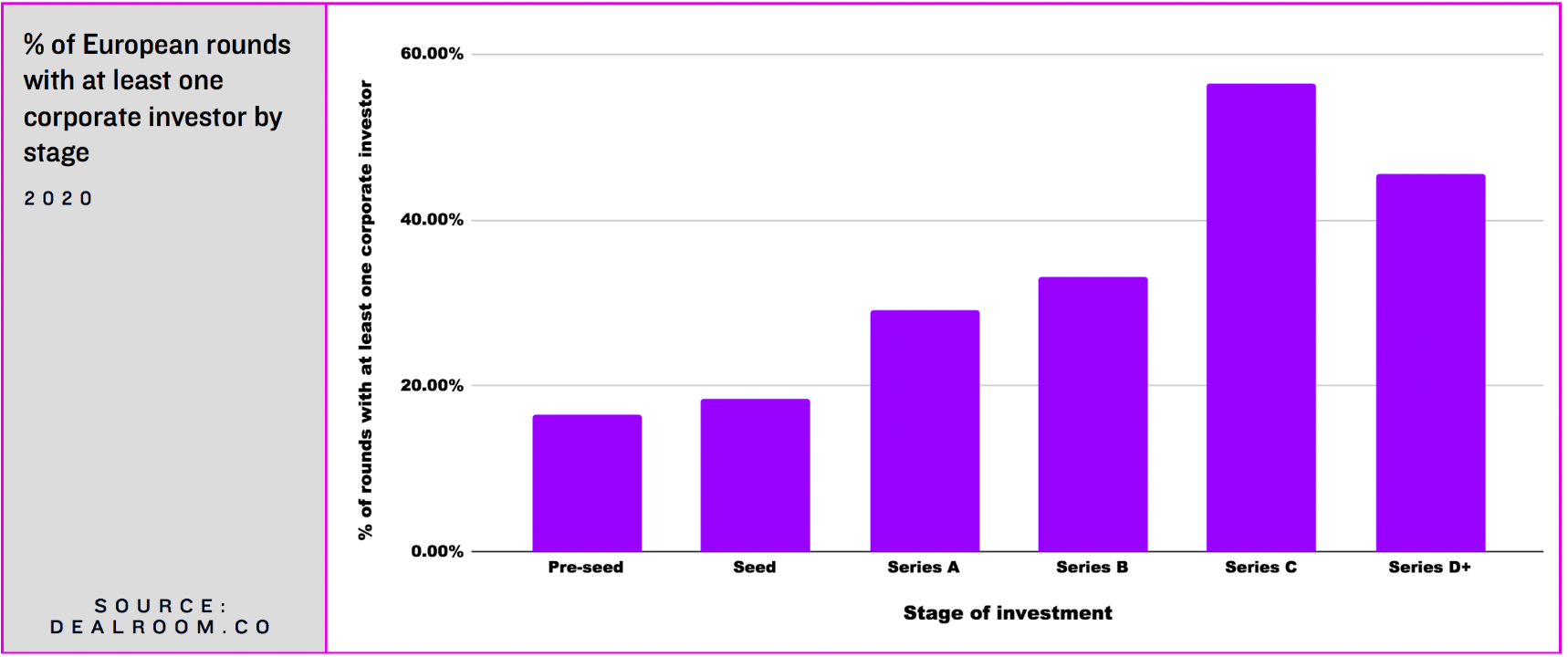

#6 Corporate investors lean towards later stages than VCs, but cash becomes a constraint

Breaking down European funding rounds by stage, we find that corporate investors are particularly important for the growth stages of the ecosystem. Last year, more than half of European Series C rounds were joined by at least one corporate backer, compared to less than 1 in 7 Pre-Seed rounds.

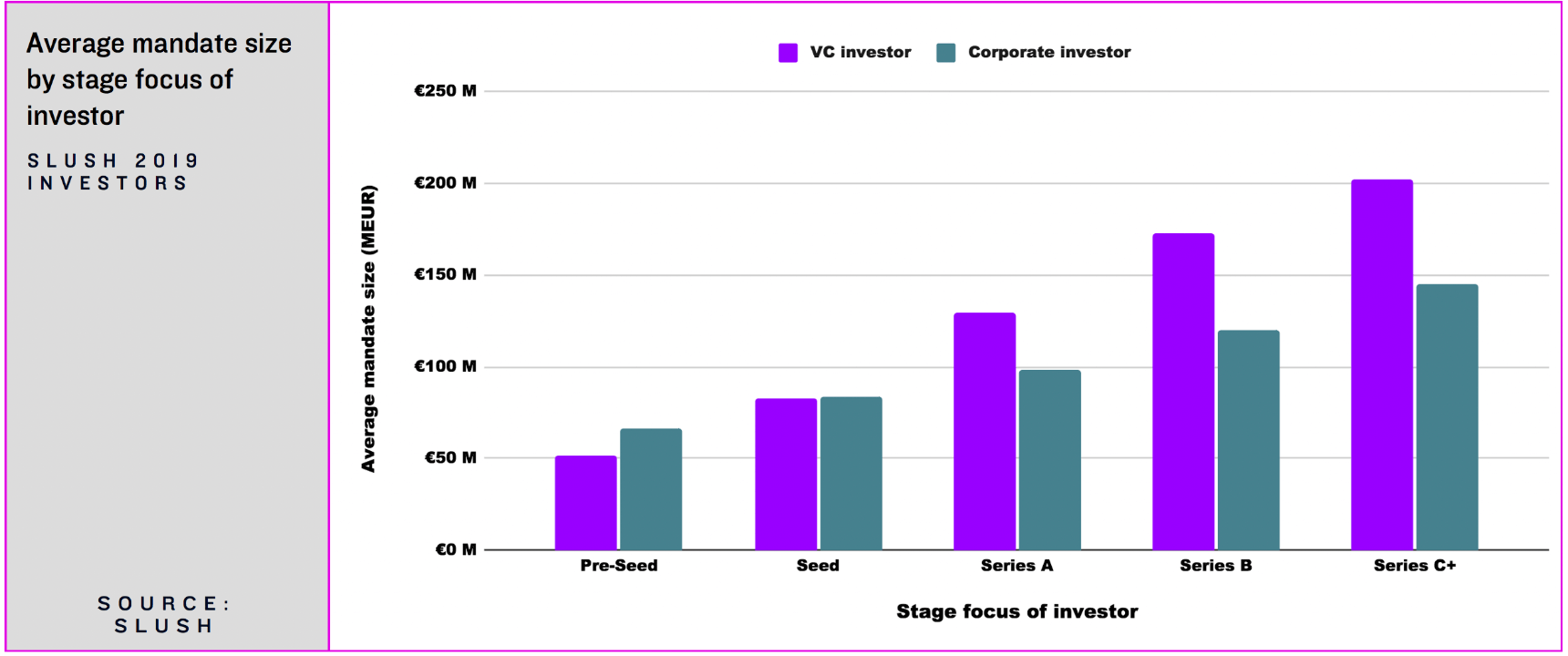

While corporate investors lean towards later-stage investments, they do seem to be held back by trailing mandate size compared to VCs. Whereas corporate investors focused on Pre-Seed and Seed at Slush 2019 reported bigger average mandates than comparable VCs, the average VC investing at Series C+ had a mandate of €203M, compared to €145M for the average corporate investor.

Our data suggest that this converts to ticket size as well. Again, while corporate investors write bigger checks up to and including Seed, the average check that a corporate investor active at Series C+ can provide is trailing the average VC by 56%.

As the amount of capital that European Growth stage companies raise continues to grow, it seems that corporate investors – particularly at Series C and beyond – will face pressure to raise bigger mandates.

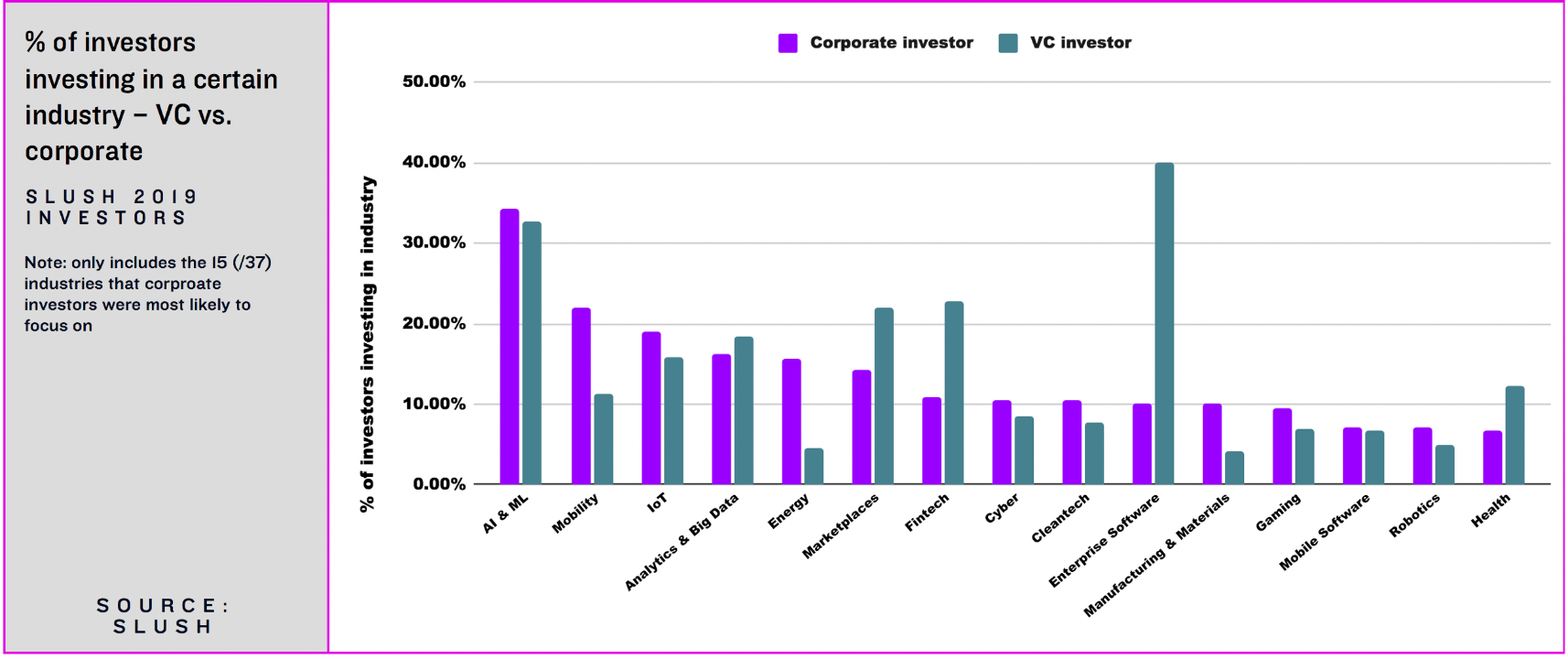

#7 Color us unsurprised: corporate investors reign in industrial verticals

Dissecting the VCs and corporate investors at Slush 2019 reveals some stark differences in industry preferences. VCs stand out as much more active in Enterprise Software, Fintech, Marketplaces, and Health. CVCs, in turn, have a significantly higher appetite for traditional or industrial verticals such as Mobility, Energy, and Manufacturing & Materials.

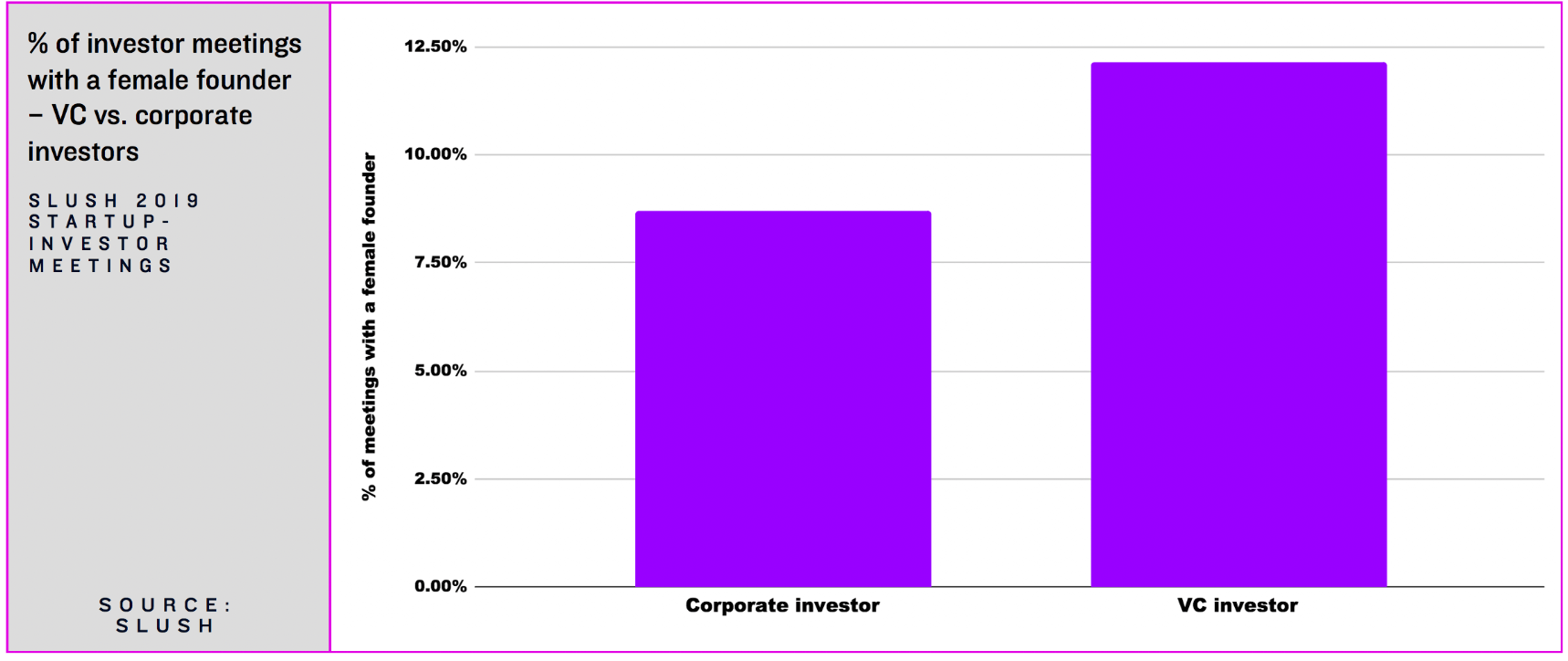

#8 Corporate investors are more gender diverse than VCs, but less likely to back a female founder

How different are VCs and CVCs in terms of their gender diversity? At Slush, 28% of CVCs were women, compared to only 20% of VCs – a striking difference.

Unfortunately, this does not convert into a higher interest in companies with female founders. While 12% of the founders that VCs met at Slush 2019 were female, women only accounted for 9% of the founders in corporate investor meetings. Needless to say, both figures are appallingly low.

The same behavior is visible across the European ecosystem. As per Dealroom, while corporate investors participated in 23.3% of European rounds in 2020, they only did so in 20.9% of rounds with at least one female founder.

This article was done in conjunction with a startup-corporate screening project funded by Teollisuuden ja Työnantajain Keskusliiton (TT-) säätiö (The Foundation of the Confederation of Finnish Industry and Employers/TT Foundation). The TT Foundation supports the competence, development, and competitiveness of industry in a sustainable way.